Slug: insurance-update-b-grade-market-fema-flood-trap

Excerpt: Florida's insurance market just earned a 'B' grade with 17 new insurers moving in, but a FEMA "flood trap" is lurking. Here is what you need to know about the 125% rate hikes.

Hey everyone, Jonathan Loescher here.

If you’ve lived in Florida for more than ten minutes, you know that the "Insurance Talk" is basically our unofficial state pastime. Usually, it’s a conversation filled with frustration, rising premiums, and the occasional "I’m moving to Georgia" threat.

But as we sit here in April 2026, the landscape is shifting. For the first time in a long time, we actually have some "good" news: at least on one side of the ledger. The Florida Insurance Commissioner recently gave our market a "B" grade. After years of barely scraping by with a "D-" or an "F," a "B" feels like we just won the lottery.

However, there is a catch. (Isn't there always?) While the standard homeowners market is stabilizing, there is a "Flood Trap" forming thanks to FEMA’s Risk Rating 2.0. If you aren't paying attention to the flood side of your policy, you might be in for a very expensive surprise.

Let’s break down what’s happening in the "B" grade market and why you need to watch your back when it comes to flood insurance.

The 'B' Grade: Why the Market is Finally Breathing

For the last few years, the Florida insurance market felt like a sinking ship. Major carriers were pulling out, and those that stayed were hiking rates faster than we could keep up. But the legislative reforms we saw back in '23 and '24 are finally starting to pay dividends.

The Commissioner’s "B" grade isn't just a participation trophy. It’s based on some real, tangible data:

- 17 New Insurers: We have 17 new insurance companies entering the Florida market. In the world of business, more players mean more competition. When companies have to fight for your business, they can’t just keep hiking rates indefinitely.

- Rate Stabilization (and even drops!): For the first time in nearly a decade, we are seeing some homeowners' insurance rates actually decrease. Some carriers have filed for rate decreases of 2% to 5%. While that’s not a massive windfall, it’s a heck of a lot better than the 25% increases we were seeing annually.

- Capital Influx: Investors are finally seeing Florida as a viable place to put their money again. This means the companies have the "dry powder" needed to cover claims without going belly-up.

This is great news if you are looking at homes in areas like Belleair Beach. It means your "standard" insurance: the stuff that covers fire, theft, and wind: is becoming more predictable.

Caption: A modern Florida home standing resilient against the elements, symbolizing the stabilizing insurance market.

Caption: A modern Florida home standing resilient against the elements, symbolizing the stabilizing insurance market.

The 'B' Grade is Only Half the Story

While I’m happy to see the market get a "B," we can't ignore the other side of the report card. While the state-regulated homeowners insurance is doing better, the federally-managed flood insurance is a different animal entirely.

If you’ve been following my blog, you know I’m a fan of transparency. And the transparent truth right now is that FEMA’s Risk Rating 2.0 is starting to bite, and it’s biting hard.

The FEMA "Flood Trap": Risk Rating 2.0

For decades, flood insurance was based on simple flood zones (A, AE, V, X, etc.). If you were in a "B" zone or an "X" zone, you were considered moderate-to-low risk and paid a pittance. If you were in a "V" zone on the beach, you paid a lot. It was binary.

FEMA changed the game with Risk Rating 2.0. Instead of just looking at a map, they now use "actuarial" data. They look at the cost to rebuild your specific home, the distance to water, the type of flooding (storm surge vs. heavy rain), and the elevation of your first floor.

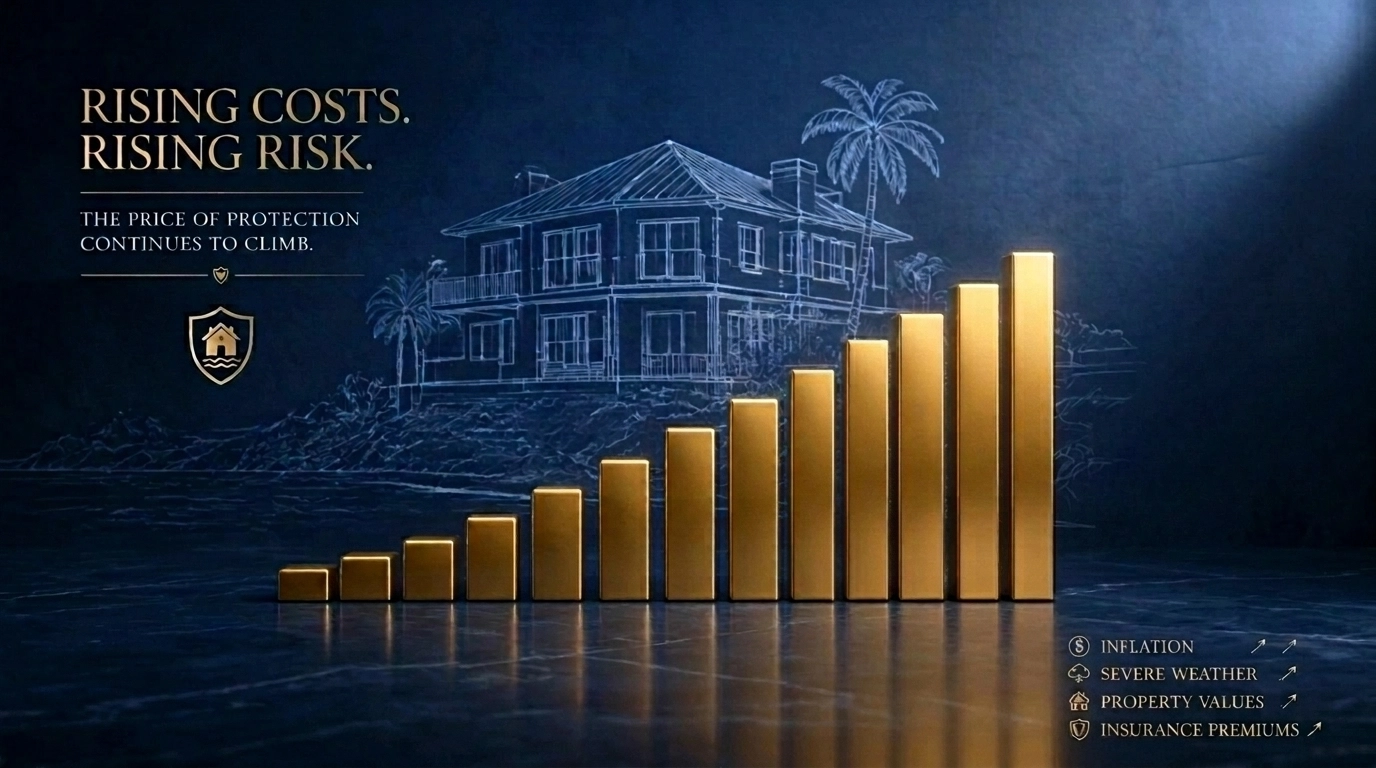

The Numbers are Scary

The projected hikes for many Florida homeowners are staggering. We are looking at projected increases ranging from +112% to +125% over the next several years for those who aren't yet at their "full risk" rate.

Because of federal law, FEMA can only raise rates on primary residences by 18% per year. That sounds "safe" until you realize that if your "true" rate is $5,000 but you are currently paying $800, you are going to see that 18% hike every single year for the next decade until you hit that $5,000 mark.

That is the FEMA Flood Trap. You buy a house thinking the insurance is affordable, only to realize you’ve signed up for a decade of compounding 18% increases.

Caption: A conceptual graph showing the steady climb of insurance premiums over a ten-year period under Risk Rating 2.0.

Caption: A conceptual graph showing the steady climb of insurance premiums over a ten-year period under Risk Rating 2.0.

Why Zone B Isn't a "Safe Haven" Anymore

The term "B Grade Market" is a bit of a double entendre here. In the old FEMA maps, Zone B described areas of moderate flood hazard. These were the areas where lenders didn't always require flood insurance.

Many buyers in places like Tierra Verde or the inland parts of St. Pete felt safe in these zones. But under Risk Rating 2.0, the "Zone" matters much less than the individual property characteristics.

I’ve seen houses in "moderate" zones get hit with higher premiums than houses closer to the water simply because the inland house was built at a lower elevation or had a crawlspace that FEMA now views as a major liability.

How This Affects Your Real Estate Strategy

If you’re working with me at Jonathan Loescher brokered by Realty of America, I’m going to tell you the same thing I tell my family: Do not trust an old insurance dec page.

When you are looking at a property, you can't just look at what the current seller is paying. You need to know what the full risk rate is.

- If the seller is paying $1,200 but the "Full Risk Rate" is $4,500, that $1,200 is a ticking time bomb.

- Once you buy the house, that 18% annual "glide path" starts for you.

This is why having an expert on your side who actually understands the insurance side of the transaction is vital. You can check out my reviews to see how I've helped clients navigate these tricky waters before.

Caption: A real estate professional reviewing complex insurance documents with a client in a casual office setting.

Caption: A real estate professional reviewing complex insurance documents with a client in a casual office setting.

Is There a Way Out?

It’s not all doom and gloom. The "B" grade in the general market actually provides an escape hatch.

As the private insurance market gets healthier (those 17 new companies we talked about), more of them are offering Private Flood Insurance. In many cases, private insurers can beat FEMA’s National Flood Insurance Program (NFIP) rates.

Because the private market is now a "B" grade: meaning it's stable and competitive: we are seeing private flood policies that are 20% to 30% cheaper than the projected NFIP full-risk rates. However, private flood isn't available for every property, and it doesn't always have the same government backing, so you have to weigh the risks.

My Advice for 2026 Homeowners

Whether you are looking to buy your dream home in Belleair Beach or you’re holding onto a property in Tierra Verde, here is your action plan:

- Get a "Full Risk" Quote: Before you close on a home, ask for the NFIP "Full Risk" rate. Don't just look at the current premium.

- Shop Private Flood: Now that the market is a "B" grade, private carriers are hungry for business. Get a quote from a private flood carrier to compare against the NFIP.

- Elevation Certificates Still Matter: Even though FEMA says they don't "require" them for Risk Rating 2.0, a good elevation certificate can often prove FEMA's data wrong and lower your rate.

- Watch the Homeowners' Side: Take advantage of the 17 new insurers. If you haven't shopped your standard homeowners' policy in the last 12 months, you are likely leaving money on the table.

Caption: A sunny coastal Florida neighborhood, illustrating the lifestyle that makes navigating the insurance market worth the effort.

Caption: A sunny coastal Florida neighborhood, illustrating the lifestyle that makes navigating the insurance market worth the effort.

The Bottom Line

We are in a weird spot. The Florida Insurance Commissioner is right: the market is getting better. We have more companies, more choices, and more stability in the standard market than we’ve seen in years. That "B" grade is earned.

But the "FEMA Flood Trap" is the hidden tax on Florida living. You have to be smarter than the average buyer. You have to look past the "now" and look at where that premium is going to be in five years.

If you have questions about a specific property or you want to know how the insurance changes are affecting home values in our area, don't hesitate to reach out. You can learn more about me and my team here.

Stay educated, stay prepared, and let’s make sure your piece of paradise doesn't turn into an insurance nightmare.

Talk soon,

Jonathan Loescher Founder, Jonathan Loescher brokered by Realty of America

Meta title: Florida Insurance Update 2026: Market 'B' Grade & FEMA Trap Meta Description: Florida's insurance market hits a 'B' grade with 17 new insurers, but FEMA's Risk Rating 2.0 brings 125% flood hikes. Learn how to avoid the flood trap. Meta Keywords: Florida insurance update 2026, FEMA Risk Rating 2.0, Florida flood insurance hikes, Jonathan Loescher, Realty of America, Tierra Verde real estate, Belleair Beach insurance, private flood insurance Florida

SEO Information

- Meta Title: Florida Insurance Update 2026: Market 'B' Grade & FEMA Trap

- Meta Description: Florida's insurance market hits a 'B' grade with 17 new insurers, but FEMA's Risk Rating 2.0 brings 125% flood hikes. Learn how to avoid the flood trap.

- Meta Keywords: Florida insurance update 2026, FEMA Risk Rating 2.0, Florida flood insurance hikes, Jonathan Loescher, Realty of America, Tierra Verde real estate, Belleair Beach insurance, private flood insurance Florida

- Publish Date: Thursday, April 30, 2026